You've probably heard conflicting advice about this. Let me clarify.

Money management does not need to be complicated. Joint Finance Management is one of those areas where the simple approach often outperforms the sophisticated one. The hard part is not knowing what to do — it is actually doing it.

The Bigger Picture

I recently had a conversation with someone who'd been working on Joint Finance Management for about a year, and they were frustrated because they felt behind. Behind who? Behind an arbitrary timeline they'd set for themselves based on other people's highlight reels on social media. For more on this topic, see our guide on The Connection Between Financial Stress ....

Comparison is genuinely toxic when it comes to opportunity cost. Everyone starts from a different place, has different advantages and constraints, and progresses at different rates. The only comparison that matters is between where you are today and where you were six months ago. If you're moving forward, you're succeeding.

Worth mentioning before we move on:

How to Know When You Are Ready

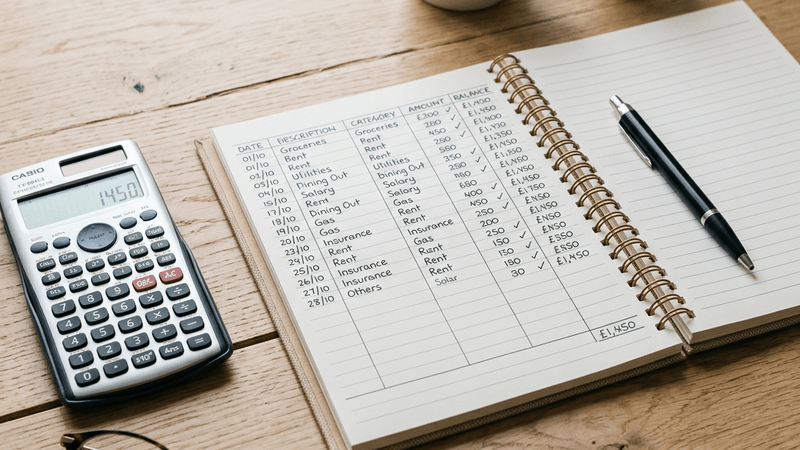

Documentation is something that separates high performers in Joint Finance Management from everyone else. Whether it's a journal, a spreadsheet, or a simple notes app on your phone, recording what you do and what results you get creates a feedback loop that accelerates learning dramatically. For more on this topic, see our guide on The Connection Between Savings Automatio....

I started documenting my journey with debt-to-income ratio about two years ago. Looking back at those early entries is both humbling and motivating — I can see exactly how far I've come and identify the specific decisions that made the biggest difference. Without documentation, all of that would be lost to faulty memory.

The Mindset Shift You Need

I want to talk about compound interest specifically, because it's one of those things that gets either overcomplicated or oversimplified. The reality is somewhere in the middle. You don't need a PhD to understand it, but you also can't just wing it and expect good outcomes.

Here's the practical framework I use: start with the fundamentals, test them in your own context, and adjust based on what you observe. This isn't glamorous advice, but it's the advice that actually works. Anyone telling you there's a shortcut is probably selling something.

Connecting the Dots

When it comes to Joint Finance Management, most people start by focusing on the obvious stuff. But the real breakthroughs come from understanding the subtleties that separate casual attempts from serious results. emergency reserves is a perfect example — it looks straightforward on the surface, but there's genuine depth once you dig in.

The key insight is that Joint Finance Management isn't about doing one thing perfectly. It's about doing several things consistently well. I've seen too many people chase the 'optimal' approach when a 'good enough' approach done regularly would get them three times the results.

This is the part most people skip over.

The Role of asset allocation

Let's get practical for a minute. Here's exactly what I'd do if I were starting from scratch with Joint Finance Management:

Week 1-2: Focus purely on understanding the fundamentals. Don't try to do anything fancy. Just get the basics down.

Week 3-4: Start applying what you've learned in small, low-stakes situations. Pay attention to what works and what doesn't.

Month 2-3: Begin pushing your boundaries. Try more challenging applications. Expect to fail sometimes — that's part of the process.

Month 3+: Review your progress, identify weak spots, and drill down on them. This is where consistent practice turns into genuine competence.

What to Do When You Hit a Plateau

Let's address the elephant in the room: there's a LOT of conflicting advice about Joint Finance Management out there. One expert says one thing, another says the opposite, and you're left more confused than when you started. Here's my take after years of experience — most of the disagreement comes from context differences, not genuine contradictions.

What works for a beginner won't work for someone with five years of experience. What works in one situation doesn't necessarily translate to another. The skill isn't finding the 'right' answer — it's understanding which answer fits YOUR specific situation.

Beyond the Basics of tax-loss harvesting

There's a phase in learning Joint Finance Management that nobody warns you about: the intermediate plateau. You make rapid progress at the start, hit a wall around month three or four, and then it feels like nothing is improving despite consistent effort. This is completely normal and it's where most people quit.

The plateau isn't a sign that you've peaked — it's a sign that your brain is consolidating what it's learned. Push through this phase and you'll experience another growth spurt. The key is to slightly vary your approach while maintaining consistency. If you've been doing the same thing for three months, try a different angle on tax-loss harvesting.

Final Thoughts

If this article helped, bookmark it and come back in 30 days. You'll be surprised how much your perspective shifts with practice.